Credit Card: Your Financial Tool

A credit card is a rectangular card, typically made of plastic or metal, issued by a bank or financial institution. It allows you to purchase goods and services on credit, meaning you borrow money from the card issuer to make the payment. You are then required to pay back the borrowed amount at a later date, either in full or in parts.

In simple terms, it's a form of short-term loan that enables you to make immediate purchases, even if you don't have enough funds in your bank account at that moment.

Key Features of a Credit Card:

Credit Limit: Every credit card comes with a pre-set spending limit known as the 'credit limit'. This limit is determined by the bank based on factors like your income, credit score, and financial history. You can only spend up to this assigned limit.

Billing Cycle: This is a fixed period, typically around 30 days, during which all your transactions are recorded. At the end of the cycle, the bank generates a statement or bill summarizing all your expenses.

Interest-Free Period: This is one of the most attractive features of a credit card. It's a grace period, usually lasting from 40 to 50 days, during which you are not charged any interest on your purchases. To avail this, you must pay the entire outstanding balance by the due date.

Minimum Amount Due: If you are unable to pay the full bill amount, the bank provides an option to pay a small portion of it, called the 'Minimum Amount Due'. However, a high rate of interest is charged on the remaining unpaid balance.

Rewards, Cashback, and Points: Most credit cards offer rewards for your spending. These can be in the form of reward points, air miles, or direct cashback. These accumulated points can later be redeemed for gifts, vouchers, flight tickets, or statement credit.

Annual Fee: Some credit cards have an annual fee for the services and benefits they offer. Many cards are also offered as "Lifetime Free," or the annual fee might be waived if you spend a certain amount within a year.

Usages of a Credit Card:

A credit card can be used for a wide variety of financial transactions:

Online and Offline Shopping: You can use a credit card to pay at physical stores, supermarkets, restaurants, petrol pumps, and on virtually all e-commerce websites and apps.

Bill Payments: It can be used to pay for your utility bills like electricity, water, mobile phone, and DTH recharges. You can also set up auto-pay for recurring bills.

Cash Advance (Cash Withdrawal): You can withdraw cash from an ATM using your credit card. However, this is generally not recommended as it attracts very high fees and interest charges from the day of withdrawal.

EMI (Equated Monthly Installment) Facility: For large purchases like electronics or furniture, you can convert the transaction amount into easy monthly installments (EMIs) to be paid over a period of time.

Pros and Cons of a Credit Card:

Pros (Advantages):

Financial Flexibility & Emergencies: A credit card provides immediate access to funds, which is extremely useful during emergencies or for unexpected expenses.

Builds Your Credit Score: Responsible usage of a credit card, especially paying your bills in full and on time, is one of the best ways to build a good credit score. A high credit score is crucial for getting loans (like home or car loans) in the future.

Security: Credit cards are generally safer than debit cards. In case of fraud, you can raise a dispute with the issuer, and you have zero liability if the fraud is proven. Your own money in the bank account remains safe.

Rewards and Discounts: You can save money through cashback, reward points, and exclusive discounts offered on travel, dining, and shopping.

Expense Tracking: The monthly statement provides a detailed record of all your transactions, which helps you track your spending and manage your budget effectively.

Cons (Disadvantages):

Debt Trap: The most significant risk is the potential to fall into a debt trap. If you only pay the minimum amount due, the high interest on the remaining balance can quickly accumulate, making it difficult to pay off the debt.

High-Interest Rates: If you don't clear your dues by the due date, the interest rates charged on the outstanding amount are very high, often ranging from 30% to 48% annually.

Hidden Fees and Charges: Credit cards can come with various fees, such as an annual fee, cash advance fee, late payment fee, over-limit fee, and foreign currency transaction fee.

Negative Impact on Credit Score: Missing payments, paying late, or using too much of your credit limit (high credit utilization ratio) can seriously damage your credit score.

Encourages Overspending: The convenience of "buy now, pay later" can lead to impulsive and unnecessary purchases, disrupting your budget and leading to debt.

In summary, a credit card is a powerful financial tool. When used responsibly and wisely, it offers great convenience, security, and benefits. However, if used carelessly, it can lead to significant financial problems.

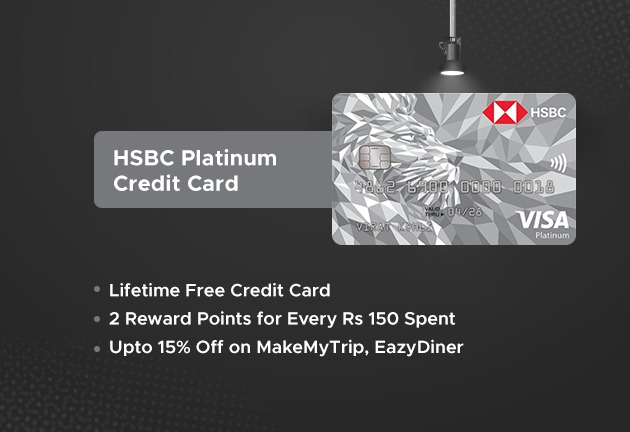

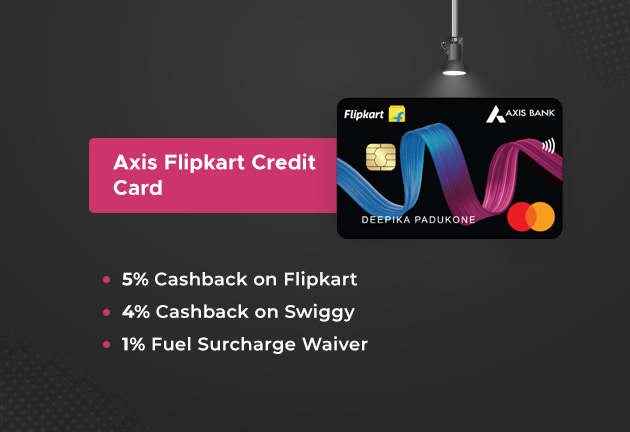

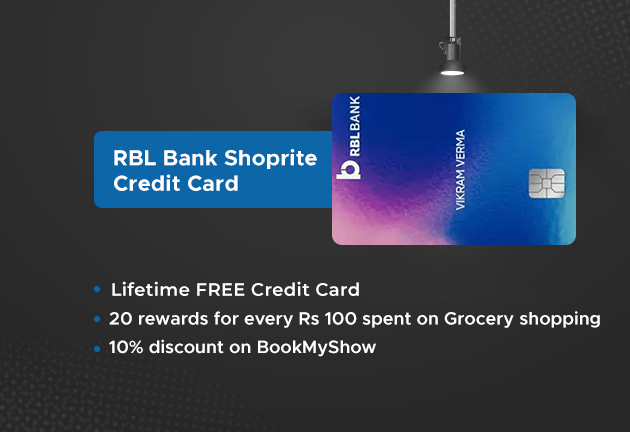

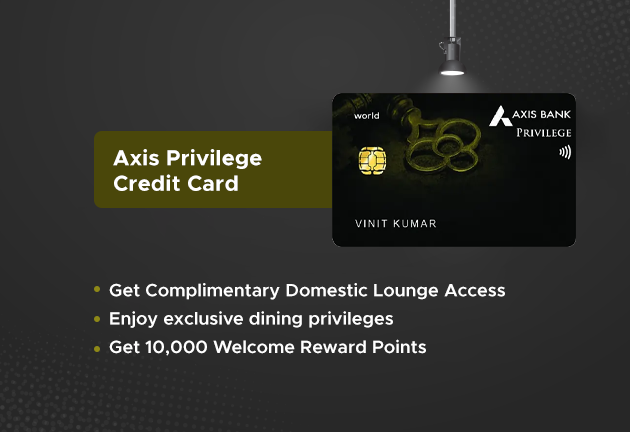

Here are some Beneficial Credit Card to buy for your Financial Needs

Online Finance Market

Your source for loans, insurance, Deposit and Investment, Stock Market .

Support

Links

contact@onlinefinancemarket.com

© 2025. All rights reserved.